Not all stocks are created equal. While some companies have the potential to soar like the next Apple or Home Depot, many others languish underperforming and fade into obscurity, if not oblivion.

Even companies that shine briefly carry the potential to dim and disappoint investors. The saga of Alibaba (NYSE: BABA) is a perfect illustration. Once hailed as “the Amazon of China,” Alibaba has experienced a spectacular loss in value, erasing nearly all the gains made since 2016. With ongoing challenges, delving into this internet and direct marketing retail stock wouldn’t make for a smart investment decision.

The Perils of Alibaba Stock Ownership

Indeed, stocks like Amazon also face obstacles and endure significant value erosion during a bear market. Savvy investors might seize the moment and acquire shares at reduced valuations. However, that isn’t my primary concern with Alibaba.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

Alibaba’s status as an international stock doesn’t necessarily set off alarms. Alibaba trades via American depositary receipts (ADRs), much like esteemed stocks such as Taiwan Semiconductor Manufacturing. Although ADRs aren’t direct ownership of foreign companies, they serve as excellent proxies for investing in overseas corporations.

My foremost reason to dodge Alibaba is the overwhelming geopolitical risk it carries. U.S.-China relations have deteriorated over recent years, placing shareholders in a precarious position. In 2022, the SEC threatened to delist several ADR companies unless they provided extensive financial disclosures. Simultaneously, the Chinese government mandated stricter confidentiality for certain company operations. Although China eventually relented and permitted disclosures, this instance serves as a cautionary tale demonstrating how seemingly unrelated political events can ravage a stock.

Another episode of political risk materialized when Alibaba fell out of favor with the Chinese government following controversial comments by then-CEO Jack Ma. In retaliation, the government imposed severe policy changes directly impacting Alibaba’s operations. These capricious actions by an almighty governing body amplify uncertainty surrounding a company, something markets detest.

Growth and the Alibaba Stock Conundrum

Moreover, Alibaba stock failed to enjoin the company’s growth. The depth of the downturn indicates problems far beyond market sentiment.

In fiscal 2014, Alibaba reported revenue of approximately 127 billion renminbi ($18 billion). By fiscal 2023, the figure swelled to 869 billion renminbi ($127 billion). Furthermore, despite market sentiment, Alibaba’s revenue rose to 459 billion renminbi ($63 billion) in the first half of fiscal 2024, translating into 85 billion renminbi ($12 billion) in non-GAAP net income, marking a 33% surge from the prior year.

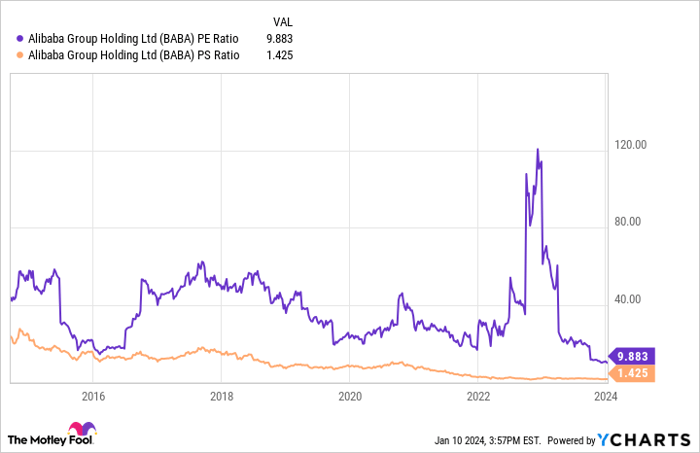

The fact that the stock barely surpasses its 2014 IPO price despite such long-term improvement is striking. Consequently, the price-to-sales (P/S) ratio, which once reached 28 soon after its IPO, has plummeted to about 1.4.

Uncertainty Surrounds Alibaba Stock

The story of Alibaba is one of the successes and pitfalls typical of big business. Despite considerable growth and a low valuation, the Alibaba stock may not be a prudent choice due to the substantial political risks it carries. Fret not for me, dear investor, for while the future may appear murky, the light of wisdom shall be our guide through these troubled waters.

Political Risks: A Cause for Concern

Alibaba’s stock, which once boasted a P/E ratio of near 60 in its infancy, now sits at a meager 9.9 times earnings. This rock-bottom valuation, however, belies the political turmoil that has besieged the company. Given the current climate, one can hardly fault investors for shying away from a stock that appears so inherently fraught with peril.

ADRs are generally viewed as safe investments; however, the recent confrontation by the SEC and the looming threat of delisting is a stark reminder of the potential hazards that come with investing in companies from nations at odds with the United States.

A Safer Bet Elsewhere

While a U.S.-based stock like Amazon may come with a higher price tag, it could very well be worth it to avoid the unnecessary political risks that come hand in hand with Alibaba stock. The assurance of stability and the avoidance of potential international crossfires is a solid argument for considering other investment options.

Therefore, in the wake of these tumultuous circumstances, wisdom might counsel in favor of pursuing other investment avenues instead of entangling oneself in the knotty quagmire that is Alibaba stock.

The Motley Fool’s Advice

The Motley Fool Stock Advisor analyst team has identified 10 stocks in which they believe investors should invest. Conspicuously, Alibaba Group did not make the cut. The stocks recommended by the Stock Advisor service are anticipated to yield substantial returns in the years to come – a compelling reason to heed their advice.

With guidance on portfolio building, regular updates from analysts, and the revelation of two new stock picks per month, the Stock Advisor service has proven to outpace the S&P 500 by more than threefold since 2002 – a testament to their astuteness.

Therefore, considering their impressive track record, aspiring investors may find prudence in heeding the advice of the Stock Advisor in their investment decisions.

Alibaba stock has undeniably fallen from grace, with the former CEO of Whole Foods Market, an Amazon subsidiary, John Mackey, not holding back on his allegiance. Likewise, the absence of any position by Will Healy in the stocks mentioned reinforces the concerns raised. While the Motley Fool recommends Alibaba Group, it appears that the cautious investor may find grounds for concern and opt for more reassuring investment avenues.