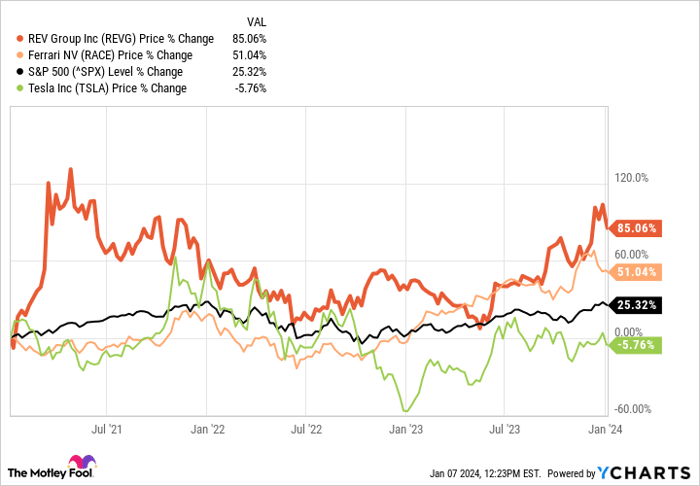

A hidden gem in the world of automotive stocks, REV Group has silently outdone established giants like Tesla and Ferrari, obliterating the S&P 500 threefold over the last three years. While not a household name, (NYSE: REVG) is a sly stock worth a look. Here’s the scoop.

Discovery of REV Group

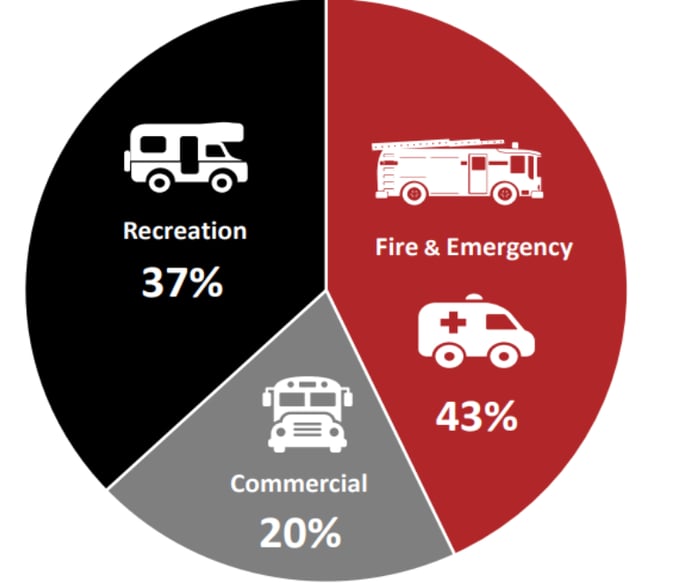

Allow me to introduce this unfamiliar company. REV Group specializes in creating and producing unique vehicles and aftermarket components and services. The company works within three primary areas: fire & emergency, commercial, and recreation.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

REV Group (REVG) TTM sales through Q3; TTM = trailing 12 months. Image source: REV Group.

When you consider public service organizations acquiring ambulances, fire trucks, school buses, transit buses, industrial sweepers, and recreational vehicles, many turn to REV Group for their requirements.

Let’s explore the company’s robust current business, a thriving backlog of orders, and a potential catalyst that may propel the stock even higher.

Mounting Orders Backlog

For an investor, few things are as comforting as a blooming backlog of orders. Such transparency in revenue is reassuring, and REV Group’s backlog confirms this at a monumental $4.5 billion.

Now let’s put that number into perspective. This backlog represents almost two years’ worth of net sales – the company’s projected net sales for the entire year of 2024 are between $2.6 billion and $2.7 billion.

Now, let’s delve into the segment fueling this strong backlog of orders.

Fervent Focus on Fire & Emergency

REV Group is currently heavily invested in the fire & emergency sector, boasting a record backlog of $3.6 billion by the end of 2023. It not only influences current results but also stands ready to steer future profits.

What’s even more appealing for investors is the improved profitability. Net sales escalated from $253 million in 2022’s fourth quarter to $339.1 million a year later. Particularly striking is the segment’s adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), which soared from $1.9 million to $26.8 million over the same period.

The uptick in profitability comes from efficiency enhancements in labor retention, increased starts and completions (essentially, refining operations and throughput), and the ability to implement price hikes.

Investors should note that REV Group’s fire & emergency segment is subject to seasonality effects, and management anticipates a typical slowdown in the first quarter of 2024 due to fewer working days.

The Recreation Uplift

REV Group’s commercial segment has remained steady in growth, witnessing a solid backlog for school buses but tepid demand for terminal trucks and street sweepers. The adjusted EBITDA margin for the category surged from 3% in the fourth quarter

REV Group: A Revival or Ride to Ruin?

Challenges in the Recreation Vehicle Industry

REV Group, a prominent manufacturer of specialty vehicles, encountered substantial headwinds in the past year. The company saw its 2023 year-end backlog dwindle by an astounding 66%, particularly in the recreation category characterized by subdued demand for towables and camper units.

The comprehensive woes did not end there. In FAUXXXXX, the company was beleaguered by a meager increase in revenue and suffered a nosedive in its market share. However, the turning point lay in its surging margins in two out of three segments, laying the groundwork for potential revival.

Strategic Shifts and Economic Resurgence

Management galvanized its will to forge a path toward fiscal resurgence through meticulous cost-saving efforts and labor retention strategies. These robust initiatives are aimed at counterbalancing the prevailing demand frailty. A glint of hope emerges with a prospective spike in recreational demand during the forthcoming spring and summer, potentially bolstering the company’s bottom line.

Assessing the Investment Proposition

Amidst this turbulent period, the pressing question for investors is whether REV Group presents a compelling investment prospect. Admittedly, expecting the company to triple the market once more in the ensuing three years is a formidable ask. Nonetheless, underneath the tumult lies the fact that REV Group is metamorphosing into a finely tuned machine, much like the vehicles it sells.

The company’s commendable price-to-earnings ratio, standing at 22 times, portrays a sound valuation. Adding to the allure is a dividend yield of 1.2%, a potential source of income growth contingent upon the company’s sustained margin upswing and a resurgence in recreational vehicle sales. The company’s backlog furnishes investors with an exceptional degree of revenue transparency that is seldom encountered in the stock market.

If REV Group fails to persuade investors of its immediate investment allure, it is advisable to keep the company under the watchful eye until serendipitous conditions permit acquiring shares at a lowered price point.

Moreover, to acquire an in-depth perspective on REV Group’s investment landscape, it is imperative to consider expert analysis and exhaustive stock evaluations. However, it is worth noting that the Motley Fool Stock Advisor team did not select REV Group among their top 10 stock picks, which may shift the outlook for potential investors.

Investors must tread with caution and scrutinize the horizon closely before making any definitive investment decisions related to REV Group.

*Stock Advisor returns as of December 18, 2023