The crypto world has been abuzz with talk of “tokenization,” especially when it comes to “real world assets” (RWAs). But underneath the hype, this trend seems to be just a rebranded version of security tokens, a concept that garnered attention back in 2018 for all the wrong reasons.

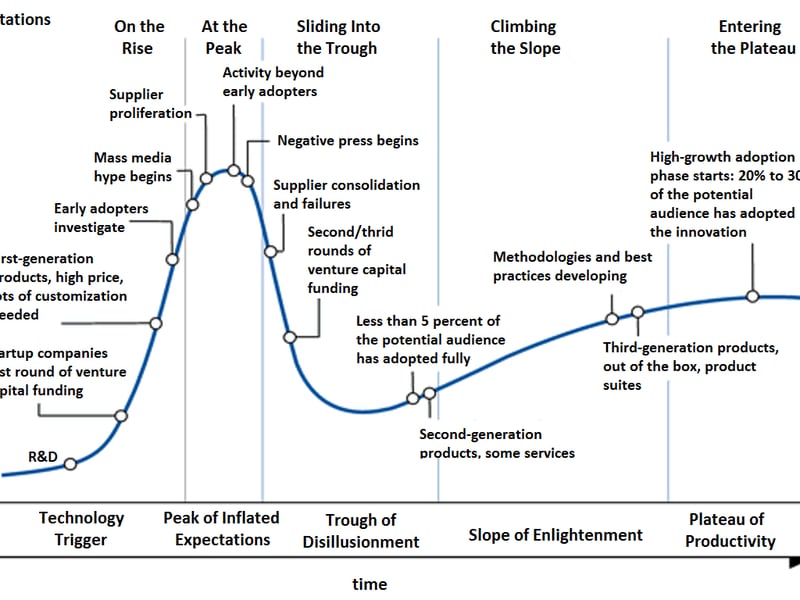

The individuals championing tokenization mean well, but it’s hard to ignore the similarities between “security tokens,” “tokenization,” and RWAs. If the Gartner “Hype Cycle” is to be believed, another downturn may be looming on the horizon.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

Those currently advocating for tokenization have mostly migrated from the previous frenzy of decentralized finance (DeFi). While traditional financial influencers view tokenization as a natural progression in finance, the complexities surrounding the tokenization of “every financial asset” are widely misunderstood by both its supporters and critics.

The fledgling RWA assets industry is now in its eighth year, which commenced in late 2017. Challenges faced during this period led firms, such as Vertalo, to shift their focus from issuing tokenized equity to becoming a provider of enterprise software that fosters connections within the digital asset ecosystem.

Subsequently, the meteoric rise and subsequent plunge of non-fungible tokens (NFTs) and DeFi have paved the way for a shift towards real-world assets. Notably, DeFi giants MakerDAO and Aave have redirected their attention to traditional financial institutions.

With astute foresight, DeFi leaders have transitioned from the governance token-airdrop model to concentrate on tokenization. This strategic move has prompted a widespread adoption of the RWA moniker and a rapid departure from anything resembling a copy-paste rug pull, a characteristic risk prevalent in the DeFi realm of 2020-2022.

However, despite the widespread excitement around RWA projects, it’s crucial to note that the assets and collateral involved are predominantly stablecoins, rather than tangible assets.

Mapping the current RWA market to the Gartner Hype Cycle places it squarely under “Supplier Proliferation” today. The fervent rush to enter the RWA business reflects the burgeoning interest in this avenue.

Tokenization of RWAs indeed presents an attractive concept. Currently, ownership of most private assets is managed using archaic data management systems, which tokenization seeks to rectify.

The Reality of Tokenization

Proponents assert that tokenization remedies the outdated data management processes prevalent in private markets. Nevertheless, while it addresses certain inefficiencies, tokenization introduces its own set of challenges. Notably, most so-called real world assets being tokenized are uncomplicated debt or collateral instruments that do not adhere to the same regulatory standards as authorized securities.

In essence, numerous RWA projects participate in a practice known as “rehypothecation,” using lightly regulated cryptocurrency as collateral to generate a form of loan. Hence, the high yields pitched by most RWA projects are primarily associated with this collateral.

Although borrowing and lending remain integral aspects of the financial landscape, the assertion that real world assets are being brought onto the blockchain is somewhat misleading. It primarily involves the collateralization of crypto assets via tokens, serving as a crucial component within the larger framework.

When industry giants like Larry Fink and Jamie Dimon discuss the tokenization of “every financial asset,” they are referencing tangible assets such as real estate, private equity, and eventually public equities. Accomplishing this feat necessitates more than just smart contracts.

Insights from Direct Experience

Having spent over seven years developing a digital transfer agent and tokenization platform that has tokenized nearly four billion units representing interests in close to 100 companies, it’s evident that mass financial asset tokenization is a multifaceted endeavor.

Firstly, tokenization constitutes a relatively simple and minor component of the process. It’s a competitive space that rapidly devolves into a commodity business due to the multitude of suppliers offering similar services.

Furthermore, the fiduciary responsibilities associated with tokenizing and transferring RWAs are of paramount importance. This underscores the significance of the ledger, as distributed ledgers furnish real advantages for tokenizing financial assets, providing the foundation for verifiable ownership and secure, error-free transaction records.

In conclusion, before succumbing to the pervasive hype surrounding tokenization, it’s crucial to reflect on past trends and consider the road ahead. Falling prey to the wrong side of the cycle might lead to an outcome akin to NFT version two.