Key Points

Amazon has made structural changes to its e-commerce business to improve efficiency and profitability.

Its highly profitable Amazon Web Services (AWS) is the world’s largest cloud computing platform.

Not to rest on its laurels, Amazon is planning to spend $200 billion this year on capital expenditures.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

- These 10 stocks could mint the next wave of millionaires ›

Amazon (NASDAQ: AMZN) has turned into one of the most well-diversified companies in the world. The e-commerce giant has become a tech powerhouse, with its hands in industries ranging from advertising to entertainment to healthcare.

Although Amazon has become something of a Swiss Army knife, its two core businesses continue to grow stronger and lead the way. They’ve both been dominant for a while, and there are no signs of that stopping in the near future. It’s why I trust Amazon to survive any market crash.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

E-commerce is becoming increasingly more efficient

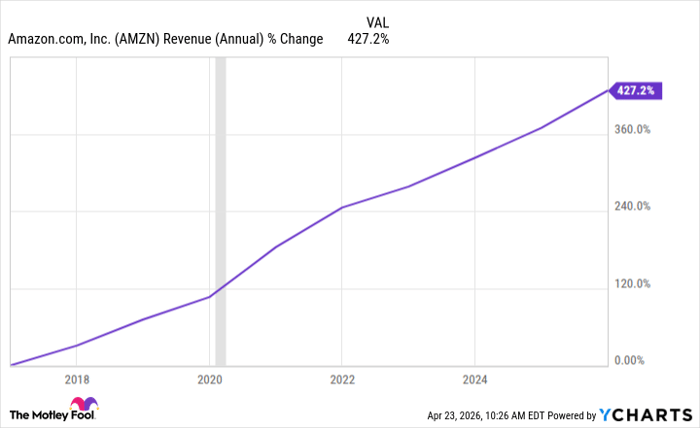

Amazon’s e-commerce business has always had an unspoken role: Bring in the revenue that Amazon can use to invest in high-growth businesses (like AWS). And it has done its job extremely well. In 2025, Amazon made $716.9 billion in revenue, more than any other public company in the world.

It’s more than just making a lot of money, though. Amazon’s e-commerce business has gotten much more efficient and profitable. Part of it is operational changes — like switching from a central fulfillment network to eight regional centers — and part of it is the introduction of more autonomous robots. In mid-2025, Amazon deployed its 1 millionth robot, which has helped increase speed and lower costs.

As artificial intelligence (AI) helps Amazon’s e-commerce and logistics businesses become more efficient, its margins should continue to expand. The once unprofitable business now has respectable margins (by retail standards). Its North America operating margins were 9% in its most recent quarter. Just a few years ago, it operated at a loss.

AMZN Revenue (Annual) data by YCharts. The vertical shaded bar represents a U.S. recession.

AWS is still the powerhouse

If e-commerce is the revenue generator, AWS is Amazon’s undisputed profit driver. It accounted for 57% of its operating income (profit from core operations) in 2025, while contributing only about 18% to its total revenue.

AWS has lost some market share with the growth of platforms like Microsoft‘s Azure and Alphabet‘s Google Cloud, but it’s still the largest cloud platform in the world. It’s sometimes called the “backbone of the internet” because many businesses rely on it to host their websites and apps.

With the growth of AI, the dependence on AWS is also growing. Amazon is planning to spend $200 billion this year building out data centers and other cloud and AI infrastructure to help accommodate the surge in demand.

Time will tell whether these ambitious spending plans translate into immediate revenue or profits, but it’s better to have the capacity to meet growing demand than to lose customers to other platforms that may be able to do so. Luckily, it has been an industry-wide predicament, which is why big tech companies are all planning to spend tens of billions this year.

Amazon recently struck a deal with Anthropic that guarantees it $100 billion in revenue over the next 10 years for providing computing capacity. Similar deals in the future likely won’t be this large, but it’s proof of just how in-demand cloud and computing capacity is during the current AI boom.

You don’t have to worry about Amazon’s long-term trajectory

In the event of a market crash, you know Amazon’s e-commerce business will remain strong. If the crash comes with a recession, Amazon still has its low prices and shipping convenience to lean on. It won’t have the physical store advantage of Walmart, but it has millions of Prime members who have “pre-paid” for delivery services and will want to take advantage of them.

Regarding AWS, its scale and high switching costs work in its favor. At this point, countless businesses have their digital ecosystem on AWS. If the market crashes or money gets tight, there’s likely a long list of things a company would cut from its budget before even considering touching AWS. This is especially true for its large enterprise clients.

Both e-commerce and AWS could experience a hiccup, but you don’t have to question whether they’ll bounce back. Amazon is a stock you don’t need to second-guess.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $540,224!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $51,615!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $498,522!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of April 27, 2026.

Stefon Walters has positions in Microsoft and Walmart. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Walmart. The Motley Fool has a disclosure policy.