Dynatrace DT is benefiting from several themes shaping enterprise software spending, including artificial intelligence, cloud complexity, platform consolidation and rising telemetry volumes.

The opportunity is clear, but not risk-free. Higher consumption can lift demand while also raising hosting costs, and DT still has to convert usage growth into annual recurring revenue and profit expansion.

Dynatrace Gains as Enterprises Cut Tool Sprawl

Enterprises are moving away from fragmented monitoring tools and toward end-to-end platforms. Dynatrace has gained from that shift, with larger and more strategic deals supporting its platform story.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

Dynatrace, Inc. Price and Consensus

Dynatrace, Inc. price-consensus-chart | Dynatrace, Inc. Quote

In the fourth quarter of fiscal 2026, the company recorded 22 deals with incremental annual contract value above $1 million, including nine new logos. That shows consolidation is not just a market slogan. It is affecting buying behavior.

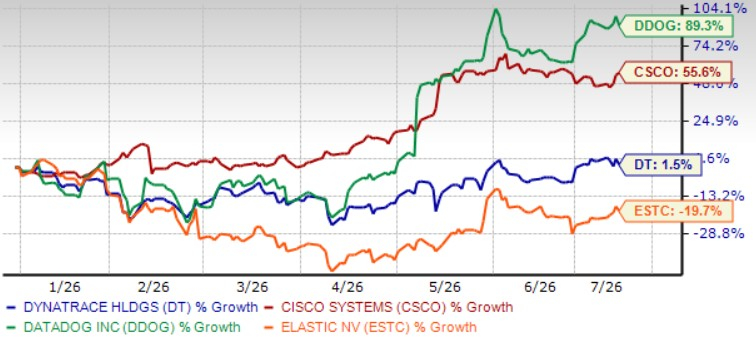

Competition remains intense. Datadog DDOG is also positioned around cloud monitoring and observability, giving investors another way to track demand for AI-era infrastructure visibility. Cisco Systems CSCO, through AppDynamics and Splunk, adds scale and breadth to the same competitive field. DT is also facing competition from Elastic ESTC.

Year to date (YTD), Dynatrace shares have appreciated 1.5% compared with Datadog’s jump of 89.3% and Cisco’s 55.6%. Elastic shares have dropped 19.7% YTD.

DT Stock’s Price Performance

Image Source: Zacks Investment Research

DT Sees AI Demand Shift Toward Autonomous Operations

Dynatrace is aligning its platform with the move from reactive monitoring to autonomous operations. Its technology combines observability data, causal context and automation to help enterprises identify problems and take action faster.

The company’s AI positioning is tied to actual workflows. More than 500 customers are deploying its agentic capabilities, while more than 850 customers are using Dynatrace to observe and trust artificial intelligence and large language model workloads in production.

Developer adoption is another part of the story. The Postman collaboration brings AI-powered observability closer to application programming interface design and testing workflows, extending Dynatrace beyond traditional operations teams.

Dynatrace is Tied to the Explosion in Logs and Telemetry

Telemetry growth is becoming a major demand driver. Logs were Dynatrace’s fastest-growing product in fiscal 2026, with triple-digit growth, and log management annualized consumption surpassed $100 million.

The planned Bindplane acquisition strengthens this angle. Bindplane is intended to improve telemetry capture, optimization and routing, helping customers manage data quality, ingest costs and governance.

That growth has a margin trade-off. Dynatrace expects about a one-point gross margin headwind in fiscal 2027 as cloud hosting costs rise with platform consumption. Management expects the pressure to be temporary, but execution on cloud cost efficiency matters.

DT Public Sector Push Opens a New Trend Line

Dynatrace is also extending its trend exposure into regulated markets. Its plan to pursue FedRAMP High authorization builds on its existing FedRAMP Moderate authorization and targets stricter government security requirements.

That push connects observability and AI adoption with compliance needs. For government and highly regulated organizations, the ability to monitor complex environments while meeting data and security standards can influence vendor selection.

This does not remove competitive pressure, but it gives DT another avenue for growth. Regulated-sector demand may support larger platform opportunities when buyers need security, visibility and governance in the same operating environment.

Conclusion

Dynatrace is a credible beneficiary of AI, cloud and telemetry growth. The company has scale, platform breadth and evidence of customer expansion, but its stock case still depends on cleaner conversion of consumption into annual recurring revenue and profits.

Dynatrace currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Dynatrace, Inc. (DT) : Free Stock Analysis Report

Cisco Systems, Inc. (CSCO) : Free Stock Analysis Report

Elastic N.V. (ESTC) : Free Stock Analysis Report

Datadog, Inc. (DDOG) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).