Any investing exposure to the “Magnificent Seven” stocks has proven successful in 2023. This group includes mega-cap tech stocks such as Nvidia (NASDAQ: NVDA), Amazon (NASDAQ: AMZN), Tesla (NASDAQ: TSLA), Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Meta Platforms (NASDAQ: META), and Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL). Surprisingly, these stocks have outperformed the broader market despite the Nasdaq Composite surging over 45% last year.

If it’s not broken, don’t fix it, right? Well, not exactly. A closer look at the numbers signals that some of these genuinely magnificent stocks could soon run out of steam. Here are the four stocks in this group worth buying in 2024, and the three to leave behind in 2023.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

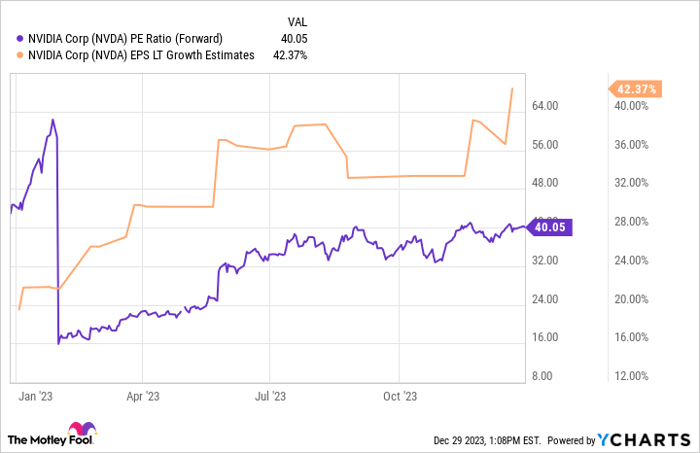

Nvidia: Seizing the Future

Nvidia’s chips, which specialize in demanding, high-compute applications, have become a focal point of the artificial intelligence (AI) breakthrough. The company has quickly established dominance, controlling as much as 90% of the market for AI chips. That’s pushed the business to new heights, accelerating revenue growth to 200% year over year in its most recent quarter to $18 billion.

NVDA PE Ratio (Forward) data by YCharts

AI demand doesn’t seem to be going anywhere, which should create plenty of growth for Nvidia moving forward. Analysts believe the company’s earnings will grow by 42% annually over the coming years, arguably justifying Nvidia’s valuation at 40 times 2023 profits. That’s a PEG ratio of just 1, signaling the stock is still attractive despite its massive 250% climb in 2023.

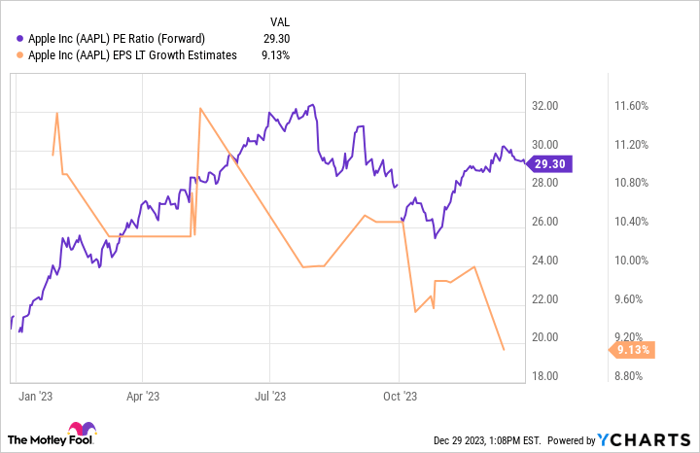

Apple: Proceed With Caution

Not every “Magnificent Seven” company has grown enough to keep up with its stock. Apple’s revenue has fallen over the past year, and net income is up just 1%. Apple’s business can be cyclical, gyrating between periods of growth depending on key iPhone releases. That’s fine, but it can complicate things when share prices and operating results go in different directions.

AAPL PE Ratio (Forward) data by YCharts

Analysts have lowered their growth expectations for Apple moving forward. At more than 29 times 2023 earnings, that PEG ratio over 3 makes buying Apple here a tough pill to swallow. Investors should wait for the price to make sense again.

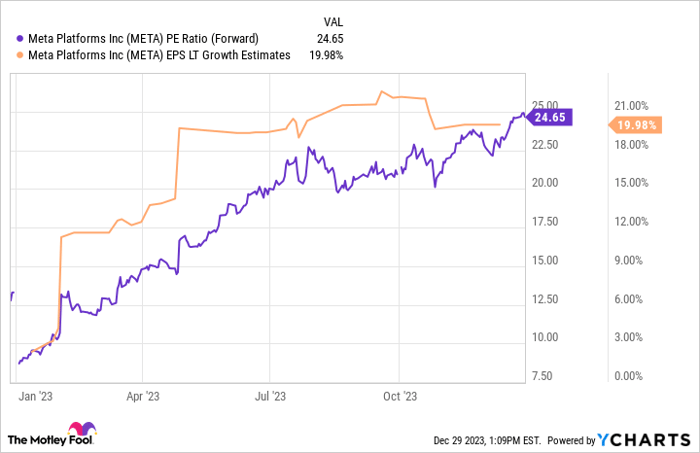

Meta Platforms: Gaining Momentum

Wall Street was down on Meta in 2022 when the company was fighting a slowing advertising business, harmful privacy changes to iPhones, and expensive metaverse projects that weren’t showing any return on investment. Shares fell to $89 before CEO Mark Zuckerberg righted the ship by cutting costs, working through the iPhone challenges, and getting revenue growth and profits back on track.

META PE Ratio (Forward) data by YCharts

Astonishingly, the stock is still attractive at just 25 times 2023 earnings, with expected annual growth of 20% on average moving forward. It turns out that Meta is still a great business, and Wall Street forgot that in a big way. The rally in 2023 undid the pessimism, but there is still room for the growth Meta can achieve in 2024 and beyond.

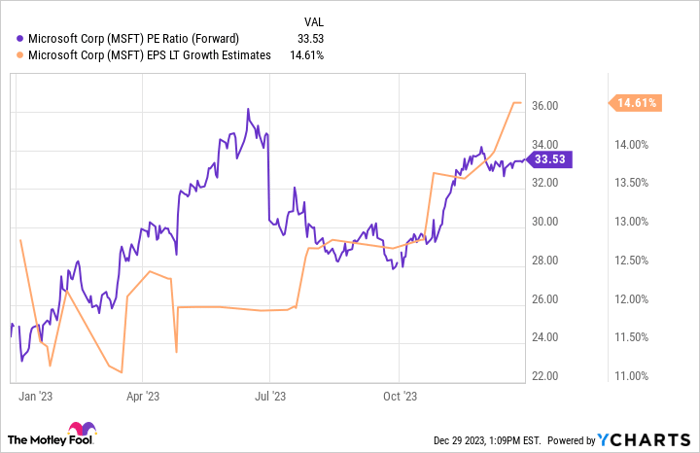

Microsoft: Be Wary

ChatGPT was a viral sensation in 2023, and Microsoft swiftly jumped in, tying itself to its creator, OpenAI, with a multibillion-dollar investment and extended partnership. Between enterprise software, cloud computing, gaming, and more, Microsoft is one of the world’s largest and most diversified technology companies. Its cloud positioning amid the AI opportunity has seemingly boosted analyst expectations for its earnings growth in the coming years.

MSFT PE Ratio (Forward) data by YCharts

Mid-teens growth is nothing to dismiss, but it’s becoming harder to call Microsoft a growth stock at its whopping $2.8 trillion valuation.

The Real Scoop on Top Stocks: Unveiling the Truth Behind the Numbers

Diving into the elite stratosphere of stock investing often feels like a trek over a financial Everest: daunting, unpredictable, and often unforgiving. Consider the stock of Nvidia, for instance. A forward P/E just over 33 might lead some investors to quickly elevate it to the summit of their portfolios. However, scratching beneath the surface reveals a resulting PEG ratio over 2, a far cry from the kind of ascension you’d expect from one of the so-called “Magnificent Seven” stocks. Sure, it’s not abhorrently expensive, but after its staggering 57% single-year sprint, there are certainly better deals to be found. It’s perfectly reasonable for investors to be discerning in the current climate.

The Amazon Angle: A Worthwhile Bet

Amazon, the e-commerce and cloud leader, finds itself alongside Microsoft with a PEG ratio just over 2. This parity may beg the question: why consider investing in Amazon over similarly valued Microsoft? The answer lies in Amazon’s history of channeling profits back into the business, a move that frequently masks its true potential take-home. Although the stock trades at a lofty 57 times bottom-line earnings, it’s a mere 22 times its operating profits, indicating a far more nuanced financial composition.

Over the last decade, Amazon’s price-to-cash-from-operations ratio stands over 20% below its average, signifying potential yet to be fully unearthed. The retail giant’s endeavors extend to cutting-edge AI technology—a pivotal piece in its future puzzle. Furthermore, with e-commerce representing only 15% of U.S. retail, Amazon’s ample room for growth is a source of prospective allure for investors.

Tesla’s Temptation: A Cautionary Tale

Tesla, a prime example of stock price and fundamentals moving in incongruent paths, recently initiated price cuts to bolster unit sales. The strategic rationale behind this move hinges on the belief that higher unit production and sales will catalyze price reductions, thereby erecting barriers that deter competitors. This bold maneuver hasn’t come without costs though—Tesla’s gross profit margin has plunged a substantial 22% over the past year.

The fervent hope is that the heightened unit sales will soon yield the cost efficiencies Tesla is chasing. Nevertheless, analysts have prudently tempered their expectations for Tesla’s future earnings growth owing to the repercussions of its price-slashing strategy. If their forecasts prove accurate, Tesla’s stock could grow increasingly steeply-priced, tipping the PEG ratio over 4. Following its remarkable 130% surge last year, investors might be better served biding their time until the numbers unequivocally validate Tesla’s strategic gambit.

The Alphabet Affair: A Lustrous Bet

Alphabet’s pervasive presence with Google and YouTube tends to obscure its latent AI potential. Hinged on leveraging AI to optimize advertising returns on its platforms, Alphabet harnesses its immense trove of user data coupled with its preeminent standing among the world’s most traversed websites to perpetuate its status as a seemingly humdrum but exceptionally efficient money generator.

In addition, the company routinely allocates a substantial portion of its cash flow to stock buybacks, effectively paring down its outstanding shares by 10% over the past five years. This amalgamation of growth and buybacks has imbued analysts with the anticipation of annualized earnings growth surpassing 17%. Despite its 57% upswing in 2023 elevating its valuation, Alphabet remains an enticing proposition for stalwart investors at a commendable PEG ratio of 1.4.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team recently pinpointed what they contend are the 10 best stocks for investors to consider right now—only Nvidia didn’t make the cut. The 10 stocks earmarked are anticipated to yield monumental returns in the years ahead. Stock Advisor equips investors with a user-friendly roadmap for success, offering insights on constructing a diversified portfolio, regular updates from analysts, and two fresh stock picks every month. Since 2002, the Stock Advisor service has eclipsed the returns of the S&P 500 by a factor exceeding threefold.

*Stock Advisor returns as of December 18, 2023