Semiconductor company Advanced Micro Devices (NASDAQ: AMD) recently unveiled its second-quarter earnings report. While its rival, Nvidia, soared with triple-digit revenue surges driven by AI demand, AMD faced hurdles in certain sectors affecting its overall sales performance.

However, there are indications of AMD’s emerging competitive edge in AI, suggesting potential for accelerated growth.

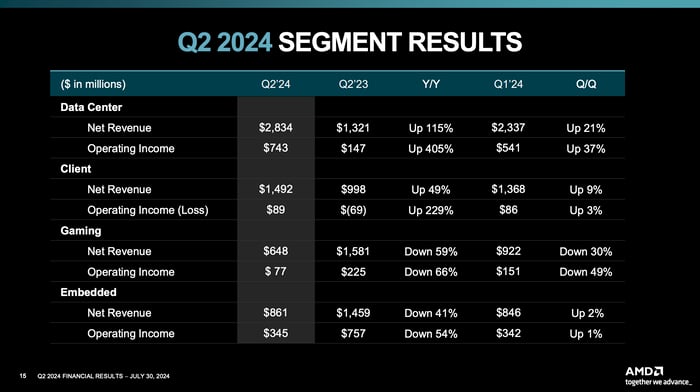

Challenges in Gaming and Embedded Sectors Impact AMD’s Growth

Despite a remarkable quarter in AI, AMD’s total revenue only witnessed a 9% year-over-year increase in Q2. Notably, plunges in gaming and embedded divisions overshadowed the robust AI growth in the data center and client segments:

Image source: Advanced Micro Devices (AMD) presentation.

The cyclical nature of the gaming sector coupled with inventory challenges in the embedded segment played significant roles in dampening sales. However, there are positive signs as the embedded revenue saw a 2% growth from Q1, indicating a potential upturn.

Despite the setbacks in gaming and embedded areas, collectively representing $1.5 billion of AMD’s Q2 sales, the company foresees an upsurge in total growth with flourishing data center, client, and embedded segments, gradually reducing the reliance on gaming revenue.

Evaluating AMD’s Versatility in AI Expansion

While Nvidia leads in AI chip market share, AMD’s progress deserves acknowledgment, suggesting significant revenue potential. With a projected $400 billion AI chip market by 2027, AMD aims to secure a substantial share, targeting around $12 billion in data center sales this year.

In Q2, AMD showcased a remarkable 115% year-over-year growth in data center revenue, outpacing the previous quarter’s 80% surge. Noteworthy mentions by Microsoft in adopting chips from AMD and Nvidia signify a trend of diversification among AI chip consumers.

The client segment, boasting a 49% revenue increase year over year in Q2, presents yet another avenue for growth. The proliferation of AI-capable PCs indicates an impending surge, with projected shipments of 600 million over the next four years.

Investors anticipate a surge in AMD’s revenue as these burgeoning segments contribute significantly to the company’s overall earnings.

Is Advanced Micro Devices Stock a Viable Investment?

While the stabilization in AMD’s embedded segment bodes well, the focus remains on its AI prospects. Robust Q2 earnings reflect a thriving business landscape, fostering confidence in AMD’s growth trajectory. Analysts predict a 33% annual growth in AMD earnings over the next few years, translating to a forward P/E ratio of 40 based on estimated 2024 earnings.

With a potential to match these growth estimates, AMD’s stock presents good value at present. The challenge lies in AMD’s ability to capitalize on its market share expansion, giving it a competitive edge against Nvidia’s entrenched position amid rising competition.

Moreover, the uptick in data center growth signals an encouraging path forward for AMD.

With multiple growth avenues available, and following a recent 30% drop in shares, believers in AMD’s ability to convert potential into tangible results may find the stock attractively priced for investment.

Considering an Investment in AMD

Prior to investing in Advanced Micro Devices, it is essential to weigh the following:

The Motley Fool Stock Advisor recently unveiled its top picks for investors, with Advanced Micro Devices not featuring on the list. The highlighted stocks are poised for substantial returns in the foreseeable future.

Reflecting on Nvidia’s inclusion in such a list back in 2005, where a $1,000 investment could have grown to over $657,306, underscores the potential for transformative growth in stock investments over time.

Stock Advisor offers valuable insights, guides on portfolio building, analyst updates, and regular stock recommendations, showcasing a significant outperformance compared to the S&P 500 since 2002.

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft.