As Chewy Inc. (NYSE: CHWY) gears up to unveil its second-quarter fiscal 2024 earnings on Aug 28, investors are eager to assess the stock’s viability as an investment option. The pet-centric e-commerce entity has captured considerable interest due to its impressive growth trajectory and strategic maneuvers. However, with the earnings event looming, the pivotal question emerges: Is Chewy a wise investment choice at this juncture?

Chewy’s ascendancy, entrenched market presence, and devoted customer base have solidified its allure among stakeholders. Projections from Zacks Consensus Estimate indicate revenues of $2.86 billion for the upcoming quarter, marking a 2.8% uptick from the previous year.

On the earnings front, the consensus view has remained steadfast at 22 cents per share over the last month, pointing to a substantial 46.7% surge year-over-year.

Image Source: Zacks Investment Research

Chewy boasts an impressive earnings track record, with an average surprise of 57.7% over the past four quarters. In the previous quarter, the company surpassed the Zacks Consensus Estimate by a substantial 47.6%.

The Trajectory of Chewy’s Price, Consensus, and EPS Surprise

Chewy price-consensus-eps-surprise-chart | Chewy Quote

Insights from Zacks Model on CHWY

Our reliable model foresees a favorable outcome for Chewy this time around. The combination of a positive Earnings ESP and a Zacks Rank of #1 (Strong Buy), 2 (Buy), or 3 (Hold) augments the likelihood of an earnings beat, a scenario that holds true here.

Chewy boasts an Earnings ESP of +4.55% and is endowed with a Zacks Rank of #2. For early access to top stocks before reporting, explore our Earnings ESP Filter.

Strategic Dynamics in Play

Chewy’s strategic emphasis on broadening its product array and enriching customer engagement likely facilitated revenue expansion. The consistent expansion of its inventory with fresh and exclusive offerings aligns with evolving customer preferences and demands. This strategy, complemented by targeted marketing campaigns and strategic promotions, is anticipated to entice new patrons while stimulating increased spending from existing ones.

The sustained success of the Autoship regimen is believed to have significantly driven revenues. As the program expands, its convenience and value are poised to elevate customer retention rates and recurrent purchases.

The introduction of the Chewy Plus membership program serves as another pivotal factor. As this initiative gains traction, the added perks such as free shipping and exclusive discounts are set to bolster higher purchase frequencies and enlarged basket sizes.

Chewy’s foray into new markets, notably its endeavours in Canada and other global sectors, hints at additional revenue growth possibilities. This diversification on a geographic scale unveils new pathways for customer acquisition. Furthermore, Chewy’s venture into veterinary services via the Chewy Health segment is geared to attract pet owners seeking comprehensive pet care. This strategic move is anticipated to unlock cross-selling opportunities and elevate customer lifetime value, thereby further fueling revenue expansion.

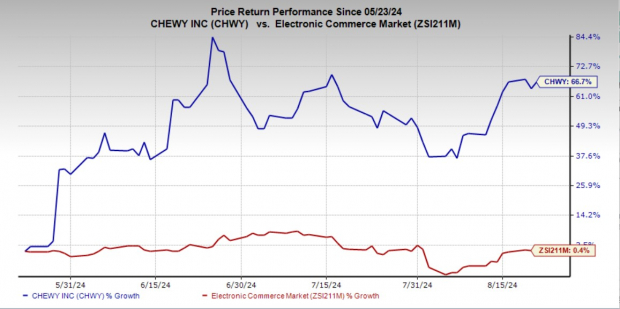

CHWY Exemplifies Dominance

Over the past quarter, Chewy’s stock has witnessed a remarkable surge, catapulting by 66.7%, vastly outshining the industry’s meagre 0.4% increase.

Image Source: Zacks Investment Research

CHWY has also eclipsed its competitors, including BARK, Inc. (NYSE: BARK), Petco Health and Wellness Company, Inc. (NASDAQ: WOOF), and Central Garden & Pet Company (NASDAQ: CENT).

While BARK shares have ascended by 43.3% during this period, WOOF and CENT have encountered declines of 10.7% and 13.7%, respectively.

Is CHWY an Alluring Proposition for Value Seekers?

From a valuation lens, Chewy shares present an enticing prospect, trading at a discount in relation to historical and industry benchmarks. With a forward 12-month price-to-sales ratio of 0.98, beneath the five-year median of 1.72 and the sector average of 1.73, the stock furnishes compelling value for investors eyeing sector exposure.

Image Source: Zacks Investment Research

Thesis on Investment

Chewy has demonstrated stellar performance, underscored by significant stock price appreciation, robust financial metrics, and strategic initiatives. Despite its recent upswing, Chewy’s shares persist in offering appealing valuation metrics alongside promising growth prospects. The company’s dedication to innovation, evidenced by the expansion of its Autoship scheme and services like Chewy Health, not only fortifies customer allegiance but also unlocks new revenue streams. Teamed with its calculated expansion into international markets and acute focus on operational efficiency, Chewy stands well-positioned to leverage the burgeoning pet care industry.

In Closing

Contemplating an investment in Chewy in anticipation of its second-quarter earnings disclosure appears logical. The company’s robust growth trajectory, underpinned by its strategic thrust on product diversification and heightened customer engagement, sets the stage for sustained prosperity. The envisaged revenue upsurge, propelled by initiatives such as the Autoship program and Chewy Plus membership, underscores the company’s knack for attracting and retaining clientele.

Furthermore, Chewy’s global market expansion and strides in the veterinary services arena bolster its long-term growth potential. With a solid track record of surpassing earnings estimates and promising signals for the forthcoming quarter, Chewy emerges as an enticing investment opportunity.