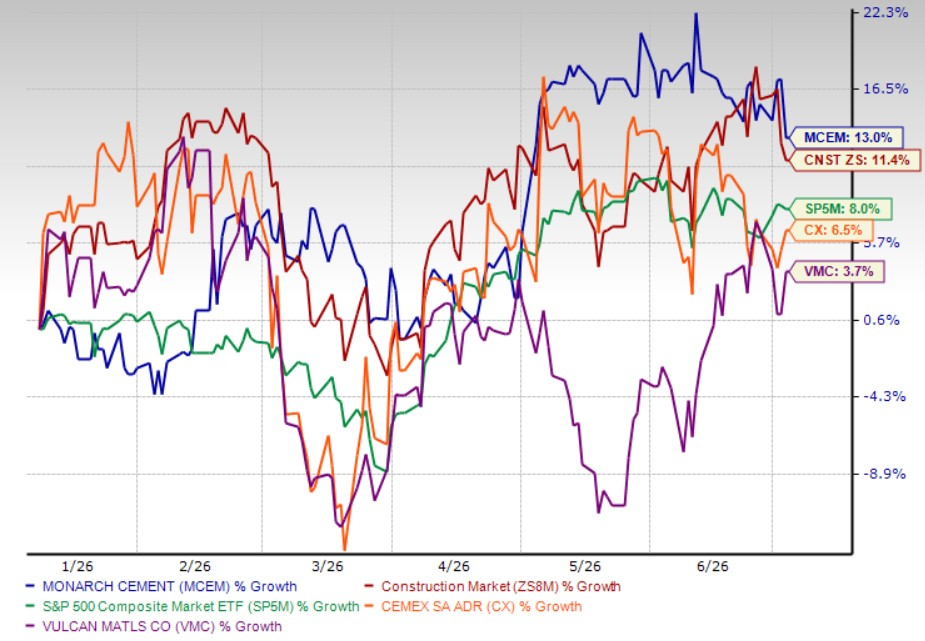

Over the past six months, shares of The Monarch Cement Company MCEM have advanced 13%, outperforming Cemex’s CX gain of 6.5% and Vulcan Materials’ VMC rise of 3.7%. The stock has also edged past the industry’s 11.4% return and the S&P500’s 8% advance during the same period, highlighting the company’s resilience in the building materials space.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

With MCEM delivering solid share price appreciation, investors are now evaluating whether the stock has additional upside. To answer that question, it is important to look beyond the recent market performance and assess the fundamental drivers supporting the company’s long-term growth prospects.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.

Key Drivers Supporting MCEM Stock

Long-Life Raw Material Reserves Strengthen Production Outlook

One of Monarch Cement’s key competitive advantages is its extensive raw material base. The company owns approximately 5,000 acres surrounding its Humboldt, KS, cement plant, with limestone and clay reserves that management estimates can support production at the plant’s current capacity for more than 50 years. The existing facility is also capable of producing more than one million tons of cement annually, while remaining well-positioned to accommodate future increases in demand.

A reserve life of this duration provides significant operational benefits by reducing raw material supply risks, limiting the reliance on third-party suppliers and supporting long-term production planning. This gives the company greater visibility into future manufacturing capacity while reinforcing its ability to serve customers over multiple decades.

Capacity Investments Position the Business for Long-Term Growth

Monarch Cement continues to invest in its production infrastructure to enhance operating efficiency and support future expansion. In the first quarter of 2026, the company invested $7.1 million in cement production facilities and an additional $4 million in routine ready-mixed concrete equipment. Management also reaffirmed plans to invest $35.2 million in property, plant and equipment throughout 2026.

The company’s Blending Silo project remains on track to become operational in Fall 2026. Once completed, the project is expected to add redundancy to the production process while reducing variability in kiln feed, resulting in improved product quality, greater operating efficiency and enhanced system reliability.

These ongoing modernization efforts should strengthen the company’s manufacturing capabilities, improve production consistency and better position Monarch Cement to meet the future demand without a proportional increase in operating costs.

Expansion Strategy Broadens Revenue Opportunities

Beyond expanding production capacity, Monarch Cement has steadily diversified its business through acquisitions, new facilities and strategic partnerships. Management highlighted the 2022 acquisition of American Concrete, the 2024 launch of a major ready-mix plant in Spring Hill, KS, and the formation of RMCMO Holdings. Under this joint venture, the company contributed several ready-mix businesses while retaining a 49% ownership interest.

These initiatives expand Monarch Cement’s presence across the construction materials value chain while increasing its regional footprint. A broader operating platform reduces the dependence on cement sales alone and provides greater exposure to construction activity through multiple product categories, supporting a more diversified earnings profile over time.

Valuation

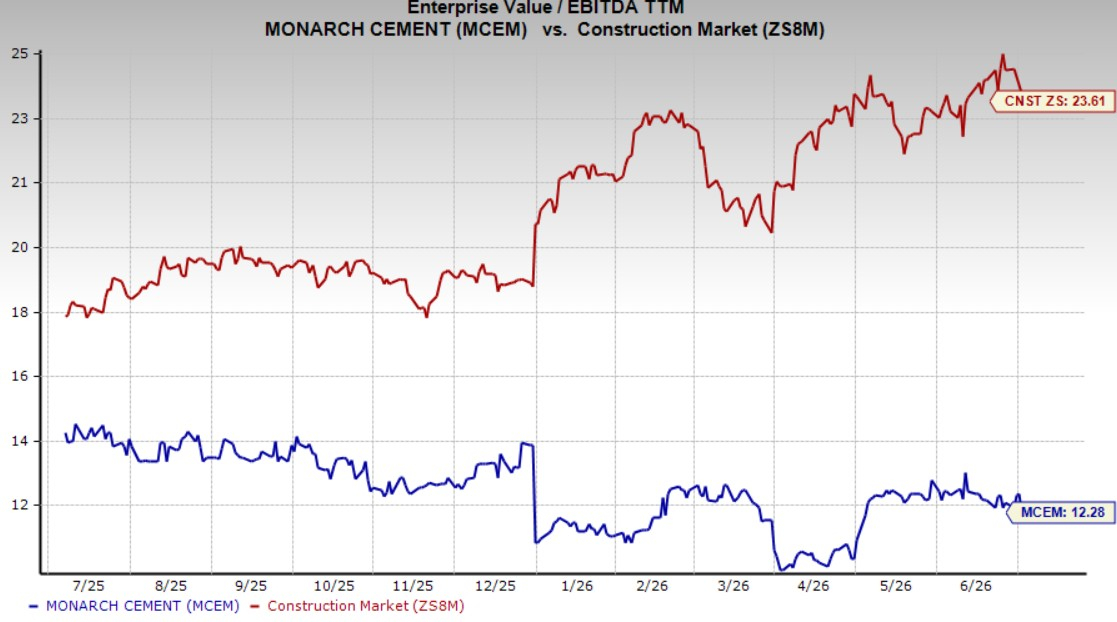

From a valuation perspective, MCEM continues to trade at an attractive level relative to the industry. The stock currently carries a trailing 12-month EV/EBITDA multiple of 12.28X, well below the broader industry average of 23.61X.

MCEM also trades at a meaningful discount to Vulcan Materials, which commands an EV/EBITDA multiple of 18.21X. While Cemex trades at a slightly lower multiple of 11X, Monarch Cement appears to offer a stronger long-term growth profile, supported by its substantial reserve base, ongoing capacity expansion initiatives and continued business diversification.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Should Investors Consider MCEM Stock Now?

Monarch Cement appears well-positioned to generate long-term value through its extensive raw material reserves, continued investment in production infrastructure and disciplined expansion strategy. These initiatives strengthen the company’s competitive position while supporting future operating efficiency and revenue diversification.

From a valuation standpoint, MCEM trades at a significant discount to the broader industry. Although its valuation is modestly above Cemex’s, the company’s growth initiatives and operational strengths make for a compelling investment case.

Overall, investors may consider buying MCEM at the current levels. The combination of attractive valuation relative to the industry, visible capacity expansion, long reserve life and strategic diversification offers favorable long-term upside for investors seeking exposure to the building materials sector.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Cemex S.A.B. de C.V. (CX) : Free Stock Analysis Report

Vulcan Materials Company (VMC) : Free Stock Analysis Report

The Monarch Cement Co. (MCEM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).