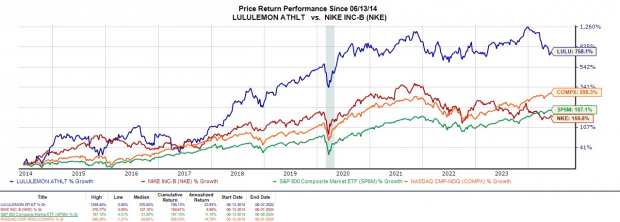

The Market Landscape

Major players in the apparel industry like Lululemon and Nike have faced challenges amidst concerns over a slowdown in consumer spending. While Lululemon’s stock has seen a decline of -8% in the past year, the company showcased resilience by exceeding Q1 revenue and earnings projections. As investors eye opportunities in the midst of Lululemon’s -37% drop year to date, the question of whether it’s the right time to acquire stock in this yoga-themed athletic apparel powerhouse lingers in the air.

Image Source: Zacks Investment Research

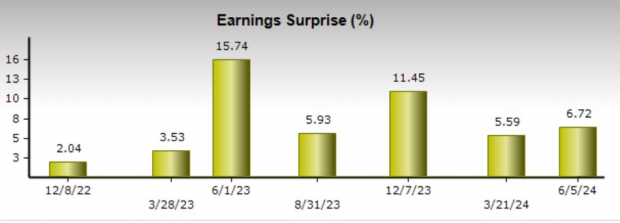

Q1 Performance & Future Outlook

Emphasizing the enduring loyalty to its brand, Lululemon reported a 10% increase in Q1 sales to $2.2 billion, surpassing estimates by a narrow margin. Additionally, Q1 EPS of $2.54 outperformed expectations by 7% and spiked by 11% from the previous year. Notably, the streak of eclipsing earnings forecasts spans 16 consecutive quarters since September 2020.

Image Source: Zacks Investment Research

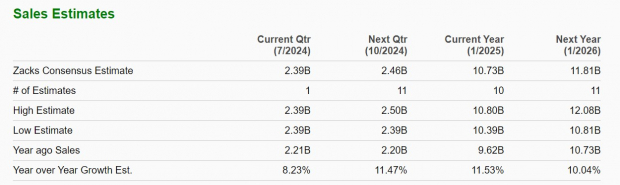

Looking ahead, Lululemon anticipates a 9%-10% growth in revenue for the second quarter, slightly above the Zacks Consensus estimate. The full-year revenue growth forecast remains between 10%-11%, with a promising expectation of 11.53% growth for the year.

Image Source: Zacks Investment Research

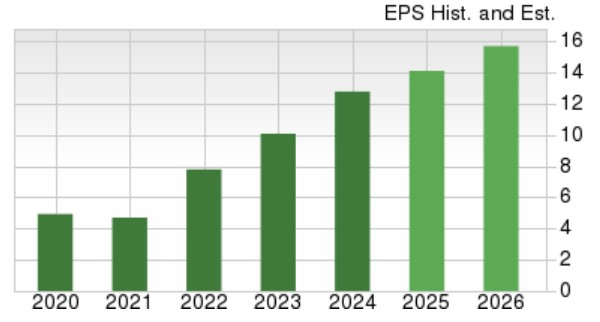

Earnings Per Share Projections

Reflecting Zacks’ estimates, Lululemon’s annual earnings are projected to climb by 11% in fiscal year 2025 to $14.14 per share, up from $12.77 in FY24. The optimism extends to FY26, with an anticipated 11% surge in EPS to $15.68.

Image Source: Zacks Investment Research

Key Takeaways

Amidst persisting concerns over consumer spending trends, especially in the premium apparel segment, Lululemon’s stock garners a Zacks Rank #3 (Hold). The robust Q1 performance underlines a promising earnings trajectory. Furthermore, trading near its lowest P/E valuation since going public, Lululemon presents an enticing opportunity for long-term investors, although the potential for better entry points remains.