Investing in stocks with visible earnings growth can be likened to nurturing a sapling with the promise of becoming a majestic oak. It’s a blend of patience and strategy that can reap significant rewards over time.

Highlighted by a few keen-eyed contributors from Fool.com, NextEra Energy (NYSE: NEE), Clearway Energy (NYSE: CWEN), and Ford (NYSE: F) emerge as promising candidates with undeniable long-term growth potential. Let’s delve into the rationale fueling their status as no-brainer buys in the current market landscape.

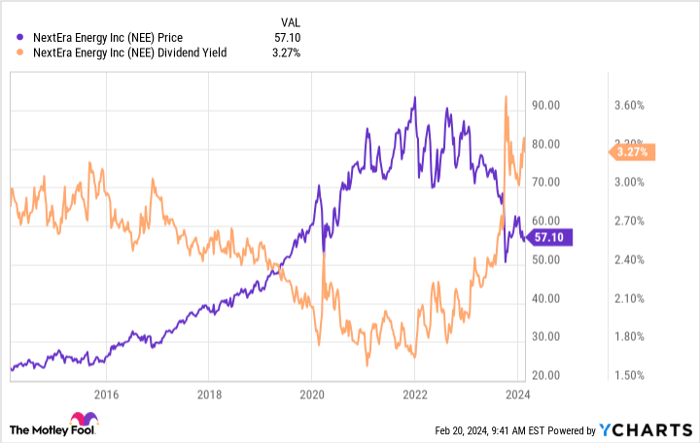

The Unique Case of NextEra Energy’s Dividend Growth

Reuben Gregg Brewer (NextEra Energy): Within the realm of utilities, NextEra Energy typically trails its peers in terms of dividend yield. Presently at 3.6%, the yield may seem run-of-the-mill for a utility, but it’s currently near its decade-high mark. This hints at a compelling valuation proposition, making NextEra Energy an enticing entry point for discerning investors.

NextEra Energy’s unique blend of a stable regulated utility component and a rapidly expanding renewable energy segment has allowed it to increase its dividend at a remarkable annualized rate of 10% over the past decade. This uncommon trait in the traditionally subdued utility sector positions NextEra Energy as an appealing choice for dividend growth enthusiasts.

Anticipated to sustain a robust 10% dividend growth rate in 2024 (with expected earnings growth of 6% to 8% yearly through at least 2026), NextEra Energy offers a glimmer of promise in a seemingly lackluster utility landscape. The opportunity to acquire a premier dividend growth utility at an attractive valuation should not be overlooked.

Unveiling Robust Dividend Growth Prospects with Clearway Energy

Matt DiLallo (Clearway Energy): Clearway Energy emerges as a prominent renewable energy producer within the national framework, prudently managing a portfolio of sustainable assets, including natural gas power plants. The stability of cash flow from its clean energy ventures, backed by fixed-rate power purchase agreements with utilities and corporate entities, serves as a solid foundation for future growth.

Maintaining an attractive dividend yield presently at 7.1%, Clearway Energy intends to enhance its high-yield payouts toward the upper echelon of its 5% to 8% annual growth target range until 2026.

The cornerstone of this growth strategy lies in Clearway’s capital recycling approach. By divesting its thermal assets in 2022, reaping approximately $1.3 billion in cash proceeds, the company redirected these funds into lucrative renewable energy initiatives. Noteworthy renewable energy undertakings in wind, solar, storage, and wind repowering projects, expected to commence operations imminently, are poised to increase power generation and augment cash flow.

With a discernible trajectory of growth beyond 2026, Clearway stands on the cusp of a promising future. Recent contract renegotiations for select natural gas power plants suggest potential support for dividend growth in 2027. Bolstered by the escalating demand for renewable energy solutions, Clearway is well-positioned to capitalize on a myriad of investment prospects, further fueled by its parent company’s expansive project pipeline.

Despite a 30% decline in shares over the past year due to market factors, the overarching narrative of substantial growth catalyzed by the renewable energy megatrend renders Clearway Energy an unequivocal long-term investment opportunity.

Stay on Course: The Ford Motor Company Trajectory

Neha Chamaria (Ford Motor): Marking an impressive uptick of nearly 19% in the past quarter, Ford’s recent financial performance underscores the automaker’s potential for a sustained bullish run.

Displaying robust figures for both the fourth quarter and the entirety of 2023 despite prevailing economic headwinds and internal challenges, Ford’s positive trajectory signals a favorable outlook for investors.

The Rise of Ford: A Financial Triumph Amidst Global Uncertainties

Ford’s Financial Turnaround

In the tumultuous year of 2023, Ford managed to steer its financial ship through choppy waters, emerging with an impressive 11% growth in revenue. This growth story wasn’t just a flash in the pan either; the company defied expectations by turning a net profit of $4.3 billion, a remarkable turnaround from the previous year’s net loss of $2 billion.

Strategic Cost Cutting and Profit Maximization

Amidst lingering uncertainties in the global market, Ford implemented strategic cost-cutting measures and reduced capital spending in sluggish markets. This laser-focused approach not only helped boost overall profit margins but also promised healthier returns for its stakeholders in 2023.

New Directions in a Changing Landscape

In a surprising twist, Ford has set its sights on trimming expenses related to electric vehicles, pivoting towards more lucrative ventures such as its commercial vehicles segment – Ford Pro. With a keen eye on sustainable profitability, Ford aims to generate adjusted earnings before interest and taxes (EBIT) between $10 billion to $12 billion in 2024, underscoring its commitment to robust financial performance.

A Promising Future Ahead

Looking forward to 2024, Ford has an exciting lineup of product launches, including a revamp of its iconic F-150 pickup truck. This strategic move not only signals Ford’s commitment to innovation but also positions the company as a solid investment option for the coming year and beyond.

As Ford continues to revitalize its operations and focus on high-growth areas, investors can rest assured that the company’s trajectory is pointing towards sustained success and value creation.